This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

From data masking technologies that ensure unparalleled privacy to cloud-native innovations driving scalability, these trends highlight how enterprises can balance innovation with accountability. These solutions are preferred for healthcare, banking and telecom industries, where stringent privacy and security standards are non-negotiable.

This process includes establishing core principles such as agility, scalability, security, and customer centricity. For example, a company aiming for market expansion might focus on developing scalable infrastructure, enabling application localization, and enhancing security measures to support operations in new regions.

Synctera , which aims to serve as a matchmaker for community banks and fintechs, has raised $33 million in a Series A round of funding led by Fin VC. In a nutshell, San Francisco-based Synctera has developed a platform designed to help facilitate partnership banking. We hope to further diversify community banks’ revenue streams.”

However, it differentiated itself by committing to payments on social media platforms, which Nigerian digital bank Carbon was interested in when it acquired the startup in 2019. As such, banking-as-a-service platforms see an opportunity to provide more personalized services and flexibility at less cost.

Founded in 2017 by Hilda Moraa , Pezesha has built a scalable digital lending infrastructure that allows both traditional and non-traditional finance institutions to offer working capital to MSMEs. Pezesha is tapping local and international banking institutions, HNWIs and DeFi for additional liquidity for onward lending.

The fintech partners with more than 220 banks in tier 2 and tier 3 cities spread through 19 provinces. Komunal digitizes rural banks, called BPRs (Bank Perkreditan Rakyat) through its DepositoBPR platform, which lets users make deposits and apply for loans digitally without needing to visit their bank’s physical location.

Add to this the escalating costs of maintaining legacy systems, which often act as bottlenecks for scalability. The latter option had emerged as a compelling solution, offering the promise of enhanced agility, reduced operational costs, and seamless scalability. Scalability. Scalability. Cost forecasting. The results?

You sit up, mind already spiralling: Do I call the bank now? Its not a humanits your banks AI-powered virtual assistant. This is the power of AI agents in actionredefining what customer experience looks like in modern banking. The Challenge: Why Banking Needs AI Agents With rapid innovation comes rising customer expectations.

Founded in 2016, Pismo has racked up a list of big-name customers, including Banco Itaú (one of Brazil’s largest banks), BTG, Cora, N26 and Falabella. Pismo’s cloud-native core processing platform is aimed at giving banks, fintechs and other financial institutions “flexibility and agility,” said Josua. Image Credits: Pismo.

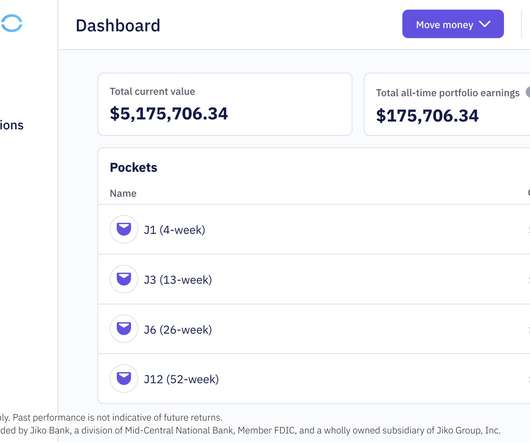

Jiko started its life as a mobile bank for consumers. Then last November, Jiko revealed it was pivoting from that consumer-focused model and “accelerating its business-to-business strategy,” as reported by Banking Dive. In 2020, Jiko made headlines by being the first fintech to acquire a nationally regulated U.S.

Tonic’s approach has the benefit of helping solve not just privacy issues, but also scalability challenges as datasets get larger and larger in size. He said that the idea for what would become Tonic originated while troubleshooting problems at a Palantir banking client. data governance) based on local privacy laws.

Datanomik’s goal is to connect financial institutions across LatAm through its B2B open finance API, which gathers a company’s banking information on one platform, Strauss told TechCrunch. “There was no easy way of interacting with our bank accounts. Datanomik co-founders Sergio Fogel and Gonzalo Strauss.

billion last year — up 153% year-over-year in terms of global VC deal value — and include a range of outfits, from payments companies to digital banks to corporate spend players. It’s not as typical for us to hear, though, about venture capitalists pouring millions of dollars into a traditional bank.

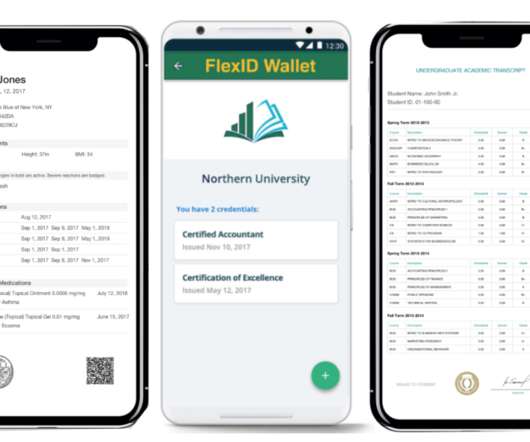

One of the startups working toward this vision is Zimbabwe’s FlexID, which is building a blockchain-based identity system for those excluded from the banking system due to their lack of identity documents. More than 60% of adults in sub-Saharan Africa are unbanked, according to World Bank estimates for 2021. million in 2016.

When orchestrated effectively, these technologies drive scalable transformation, allowing businesses to innovate, respond to changing demands, and enhance productivity seamlessly across functions. AI in action The benefits of this approach are clear to see. 4] On their own AI and GenAI can deliver value.

For banks, data-driven decisions based on rich customer insight can drive personalized and engaging experiences and provide opportunities to find efficiencies and reduce costs. Embrace scalability One of the most critical lessons from Bud’s journey is the importance of scalability. They can be applied in any industry.

And yet, “the main source [of funding] for them right now is the traditional banking system. Banks in developed countries are focused on supply chain finance for large countries and banking systems in developing markets are still underdeveloped. trillion and will grow to $6.1 “They could be a barbershop.”

Mohamed Salah Abdel Hamid Abdel Razek, Senior Executive Vice President and Group Head of Tech, Transformation & Information, Mashreq explains how the bank is integrating advanced technologies and expanding its digital footprint. This approach has significantly enhanced the customer banking experience.

AI practitioners and industry leaders discussed these trends, shared best practices, and provided real-world use cases during EXLs recent virtual event, AI in Action: Driving the Shift to Scalable AI. And its modular architecture distributes tasks across multiple agents in parallel, increasing the speed and scalability of migrations.

a banking-as-a-service (BaaS) platform that aims to build “DeFi for traditional finance,” has raised $16 million in a Series A round of funding led by CM Ventures. From a product architecture standpoint, Productfy has been built “from the ground up,” he said, to operate with multiple banking partners. Productfy Inc. ,

The round was led by Pan-African early-stage venture capital firm, TLcom Capital , with participation from nonprofit Women’s World Banking. So the startup instead partners with banks. Banks provide loans to farmers and make it compulsory for them to have insurance. Image Credits: Pula. The pair both act as co-CEOs. ”

Bank over the years is that effectively deploying and making use of new tools requires a skilled and diverse workforce and a technology team with a strong engineering culture to support it. Banking on technology and people The largest technology investment for U.S. What we have discovered in implementing emerging technology at U.S.

How has banking evolved during the rapid digitisation of recent years? Banks are no longer the key players in the market, with fintech companies, digital-first start-ups, and tech giants delivering their own brand of financial services. One example is Banking-as-a-Service, with the market expected to reach US$3.6

How has banking evolved during the rapid digitisation of recent years? Banks are no longer the key players in the market, with fintech companies, digital-first start-ups, and tech giants delivering their own brand of financial services. One example is Banking-as-a-Service, with the market expected to reach US$3.6

Blockset’s clients include some of the largest ATM networks and Japanese investment bank (and BRD investor) SBI Holdings, CoinFlip, Welthee, CoinSwitch, Coinsquare and Wyre. If you’re a financial institution, you can’t accept anything other than instant, accurate and highly-scalable kinds of data.

For instance, at the National Australia Bank, it’s reported that half of the production code is generated by Q Developer, allowing developers to focus on higher-level problem-solving. ” Use AI for rapid prototyping, but it’s your expertise that transforms raw output into robust, scalable software.

The new funding was led by Alkeon Capital, an American investment firm, and included participation from new investors like Korea Development Bank, and returning backers Altos Ventures and Greyhound Capital. Toss Bank will be able to offer better rates because its risk-scoring model leverages data from its millions of users.

Similarly, the financial sector will see continued growth in fintech, digital payments and open banking, with cities like Dubai and Riyadh becoming central fintech hubs in the region.

The emergence of super-apps offers a unique opportunity for leaders in banking and payments to innovate and expand their reach. Financial institutions can tap into new demographics, prioritizing convenience and seamless banking application experiences. The trend is most pronounced in financial services and payments.

He began his Silicon Valley career as an investment banking analyst at Robertson Stephens & Co. during the first internet boom (and bust!). He earned his bachelors degree from Duke University , studied at University College London , and received an MBA from the UCLA Anderson School of Management.

The banking landscape is constantly changing, and the application of machine learning in banking is arguably still in its early stages. However, banks using AI and ML are quickly going to overtake their competitors. Machine learning solutions are already rooted in the finance and banking industry.

The Bengaluru-based startup offers banking and payments APIs that allow development of fintech products such as banking, payment cards, neobanking and collections and payout services in a short period of time. And it purely has to do with the bank processes, the way the bank runs the process, as well as the tech of the bank.

Tabor explained that the e-commerce landscape in Latin America was consolidated, meaning few banks controlled more of the market. In the U.S., that score is used to determine if the purchaser is legit, but they didn’t implement that in Latin America,” he added. “The

Enterprise technology leaders discussed these issues and more while sharing real-world examples during EXLs recent virtual event, AI in Action: Driving the Shift to Scalable AI. Strong domain expertise, solid data foundations and innovative AI capabilities will help organizations accelerate business outcomes and outperform their competitors.

Leal, senior vice president and CIO of Vantage Bank in San Antonio, Texas, said IT will replace network switches, access points, and firewalls, and the plan was to divide the project into smaller phases. The project will still be spread out through 2025, but were doing the capital outlay all at once.

2023 has commenced, and rates are climbing, inflation is bubbling, and banking customers are continuing to demand hyper-personalized products and experiences from their institutions. Here are five banking trends we’re forecasting for the new year. Three prominent areas where there is a strong desire to optimize: Data.

Formerly known as the Commonwealth Development Corporation, the BII is not alone: The World Bank’s International Finance Corporation (IFC) and the Netherlands’ Dutch Entrepreneurial Bank (FMO) have each invested in more than 10 startups over the last four years.

Recently, I attended the 2023 Bank Automation Summit , where one of the significant topics of discussion was how banks navigate their transition to the cloud. Cloud computing makes data more accessible, cheaper, and scalable. The computing and storage of cloud data occur in a data center, rather than on a locally sourced device.

Volopay, founded by Shaji and the startup’s chief technology officer Rajesh Raikwar , wants to disrupt traditional business banking and offer companies a control center for all their financial management needs without the hassle and limitation of a traditional bank. .

s FCA and Bank of England; the National Bank of Rwanda in Africa; as well as the ASIC, HKMA and MAS in Asia. Several “super regulators” are also engaged in suptech efforts such as the Bank of International Settlements, the Financial Stability Board and the World Bank. But what exactly is suptech?

Greater integration and scalability: This modular architecture distributes tasks across multiple agents working in parallel, so Code Harbor can perform more work in less time. Banks see faster migrations Enterprises in the financial services industry are already reaping the benefits.

According to a Bank of America survey of global research analysts and strategists released in September, 2024 was the year of ROI determination, and 2025 will be the year of enterprise AI adoption. Vendors are adding gen AI across the board to enterprise software products, and AI developers havent been idle this year either.

Petabyte-level scalability and use of low-cost object storage with millisec response to enable historical analysis and reduce costs. For example, a bank should be able to see separate views of the performance of its ATM and online banking systems. A single view of all operations on premises and in the cloud.

These agents, from different parts, then proceed to make lump-sum payments into a central bank account. With Duplo, distributors can create unique virtual accounts for retailers and agents to make real-time payments or bank transfers, while the platform helps to reconcile their books automatically.

We organize all of the trending information in your field so you don't have to. Join 49,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content