This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the face of shrinking budgets and rising customer expectations, banks are increasingly relying on AI, according to a recent study by consulting firm Publicis Sapiens. Around 42% percent of banks rely on personalized customer journeys to improve the customer experience.

Bank of America will invest $4 billion in AI and related technology innovations this year, but the financial services giants 7-year-old homemade AI agent, Erica, remains a key ROI generator , linchpin for customer and employee experience , and source of great pride today.

Beyond Bank Australia is one of the largest customer-owned banks in Australia and one of the leading B Corps in the country. Beyond Bank has a real focus on customers who are the members and owners of the bank. Beyond Bank has a real focus on customers who are the members and owners of the bank.

After several slow quarters, were seeing a pick up in funding to digital banking startups. billion into a geographically dispersed group of online banking providers, Crunchbase data shows. Tyme, which offers digital banking in South Africa and the Philippines, picked up the next-largest round: a $250 million Series D.

Known for its innovations in the payments sector, Square is now officially a bank. Nearly one year after receiving conditional approval , Square said Monday afternoon that its industrial bank, Square Financial Services, has begun operations. Lewis Goodwin had been tapped to serve as the bank’s CEO, and Brandon Soto its CFO.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Last month, Varo Bank celebrated the two-year anniversary of obtaining its national bank charter. consumer bank. The startup launched its banking services in 2017, aimed at making younger consumers comfortable doing all their banking online. Our largest reduction in spend is coming from marketing.

Kuda , the challenger bank based in Nigeria and the U.K., Kuda, the African challenger bank, raises $55M at a $500M valuation. Per sources, this includes growth, marketing and product departments. has joined the ranks of tech companies in Africa that are pruning their workforce. billion, cut 15% of its staff in June.

IT leaders must understand how the business plans to compete, grow, and create value in the market to align IT initiatives within the company’s broader objectives. By staying ahead of market trends, the organization remains agile, adaptable, and ready to outperform rivals. Learn more about IDC’s research for technology leaders.

The Scotts Valley, California-based company is using cloud technology and the Ethereum blockchain as the engine for its Paystand Bank Network that enables business-to-business payments with zero fees. On the commercial side, however, one business trying to send $100,000 the same way is not as easy. Paystand wants to change that.

Like other data-rich industries, banking, capital markets, insurance and payments firms are lucrative targets with high-value information. To discuss these and other security issues faced in this market, David Moulton, director of content marketing for Cortex and Unit 42, chatted with a few Palo Alto Networks experts.

It may go down in the history books about Silicon Valley: the time that its most prominent bank, a bank founded nearly 40 years earlier, inflicted such grievous injury on itself that it had to be rescued by another bank or else risk going down in flames in a single day. Not because the bank is falling apart at the seams.

Different demographics often have different banking needs. So it’s no surprise that we have seen a flurry of financial technology startups offering banking services catered to certain populations based on factors such as age and ethnicity. Like many fintechs, Charlie is not a bank — its banking partner is Sutton Bank.

The United States has been trying to counteract the popularization of technological solutions from China for years, often taking steps that are contrary to the development of an open market. China is not remaining passive and is increasingly overcoming American sanctions by gaining new market segments.

The sudden collapse of Silicon Valley Bank , which served as lifeblood for startups , is also impacting firms 8,000 miles away. Regulators stepped in Friday to shut down Silicon Valley Bank, the 16th largest in the U.S. and the bank for most startups. venture firms such as Y Combinator. Some SaaS firms are registered in the U.S.

India’s central bank has enforced several measures to cool down high growth in consumer credit in a move that will impact consumer spending and many startups in the South Asian market, industry executives said.

That includes expanding into new markets before you and your business are ready. First, you must have a successfully proven product-market fit in your current market. Entering new markets is always more expensive and slower than you expect, so its always better to have extra money set aside for this kind of experimentation.

Although 2024 was another exceptionally lackluster year for new public offerings, the IPO market could gain momentum in 2025 after its three-year lull. With that in mind, here are 13 companies that the Crunchbase News team thinks could be top contenders to go public if our 2025 market forecast bears out. That made sense.

Digital bank Chime confirmed today that it is laying off 12% of its workforce, or about 160 people. According to an internal memo obtained by TechCrunch, Chime co-founder Chris Britt described that the move was one of many that would help the company thrive “regardless of market conditions.” billion two years ago.

A 2019 World Bank report says 85% of Africans live on less than $5.50 The company, which enables underbanked customers in select African markets to access a broad range of products and services without collateral or a guarantor, announced today that it has raised $75 million.

Ivella , a Santa Monica-based startup, wants to build banking products for couples to take away some of these tensions. “The place that a lot of people fall short, just like a lot of fintech falls short, is that they don’t break the mold of what banking looks and feels like,” Lalji said.

Africa is the world’s third fastest-growing crypto market, with crypto adoption increasing by more than 1,200% over the last two years. Then, due to local bank card limitations of $20 monthly spend, we provided virtual dollar cards for Nigerians to make international purchases.”. CEO Ruth Iselema.

Michael Beckley Contributor Share on Twitter Michael Beckley is a co-founder and CTO of Appian , where he drives the technical vision for the company, leads product and solutions marketing teams, and oversees customer initiatives. Or, the UK’s Financial Conduct Authority fining GT Bank £7.8m for AML failures.

Jia, a blockchain-based fintech providing loans to micro and small businesses in emerging markets, has raised $4.3 The fintech plans to use the funding to double down on its operations in Kenya, and the Philippines, before exploring new markets in West Africa, Latin America, and Asia.

In addition to having a little over a hundred businesses like Carbon, Aella Credit, Credpal, Renmoney, Autochek, and Inflow Finance access customers bank account for bank statements, identity data, and balances , Mono has also connected over 100,000 financial accounts for its partners and analysed over 66 million financial transactions so far.

The agent bandwagon Theres a lot of agent-washing in the IT industry right now, says Chris Shayan, head of AI at Backbase, a banking software vendor. Many solutions being marketed as agents are actually just traditional algorithms with better interfaces, and theres a world of difference that CIOs and CTOs are struggling to navigate.

Among them: Banking: Organizations are delivering personalized solutions with recommendations and enhancing customer service operations with avatar-assisted services and Natural Language Processing (NPL) chatbots that fulfill service requests promptly.

Better.com finally went public The biggest fintech news of the week centered around Better.com’s no good, very bad public market debut. But I’m not sure anyone expected it to be hovering at a share price that gave Better.com a market cap of just $19.14 To sum it up, digital mortgage lender Better.com made its public debut on August 24.

It’s been only six months since Union54, whose API allows African software companies to issue and manage their debit cards without needing a bank or third-party processor, announced its seed round of $3 million, also led by Tiger Global. According to Wiki , any bank or eligible fintech can become a member.

Ash Lilani, managing partner at Saama Capital, one of Zeni’s earliest and largest investors, said he knew how big the total addressable market was — $200 billion — and how much these kinds of financial services were a giant pain point for startup companies. “To Zeni fits with that.”. I believe we have the opportunity to build a large company.

However , they seem to be doing quite well compared with traditional banks that face challenges like legacy cost structures and a major lack of operational efficiency. It is one of the few companies that builds proprietary solutions for these financial institutions and their banking and payments services.

Innovation can be internal and help change the way an organisation operates – or external and focused on meeting market growth aspirations. This can include new capabilities and competencies or employee talent programmes and market initiatives. It can also include new digital products and services.

They are responsible for communication between banks and fintechs to settle transactions for consumers and businesses swiftly. Telecoms and banks lead the majority of online financial transactions carried out in the region via mobile money wallets and bank accounts. It doesn’t aim to replace mobile money or banks.

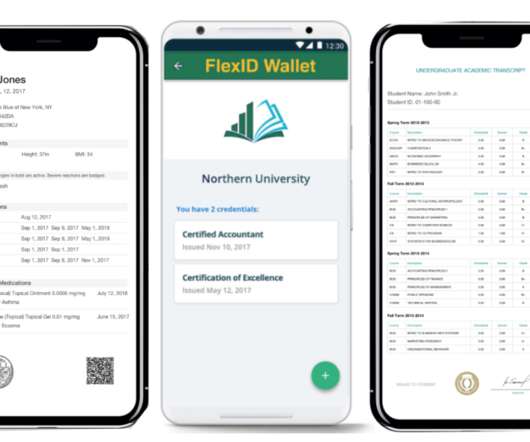

One of the startups working toward this vision is Zimbabwe’s FlexID, which is building a blockchain-based identity system for those excluded from the banking system due to their lack of identity documents. More than 60% of adults in sub-Saharan Africa are unbanked, according to World Bank estimates for 2021. million in 2016.

In the region, less than 25% of adults have bank accounts as the focus for banks remains the top 10-20% wealthiest customers. The rest, which is a huge segment of the market of about 100 million people, is not perceived as profitable. But as banks slacked, mobile money from the region’s telcos filled in the gap.

How does a business stand out in a competitive market with AI? Keeping Data Governance at the Core of Effective AI Data falling into the wrong hands should be a concern of any business—regardless of size or status in the market.

A high-street bank in the UK shows just how necessary it is to tackle the challenges that modernisation poses systematically. This makes their work easier and reduces new applications’ time-to-market. The prioritisation and implementation of steps have to be adapted accordingly in order to achieve specific business objectives.

Mono , an African startup that helps connect consumers’ bank accounts to financial applications, has raised a $15 million Series A round, the company confirmed to TechCrunch today. T hink of what Flutterwave and Paystack have done with cards; Mono wants to do with bank accounts.

By Bo Ilsoe The future of European innovation depends on a single, unified Pan-European stock market. Companies linger in the private sphere for extended periods as Western IPO markets stagnate and capital gravitates toward venture funds. A fundamental shift is imperative to revitalize this engine of innovation.

Today, the company is announcing that it has closed $9 million in seed funding to scale its operational presence, recruit talent and expand into new markets. The company is led by CEO Nikolai Barnwell , betPawa’s former head of New Markets, Africa. Typically , they would be required to use a bank account or card.

Once synonymous with a simple plastic credit card to a company at the forefront of digital payments, we’ve consistently pushed the boundaries of innovation while respecting tradition and our relationships with our merchants, banks, and customers. Back then, Mastercard had around 3,500 employees and a $4 billion market cap.

But over time, it began to focus on bigger clients and signed up a bank as its first main enterprise customer. It’s a typical salary structure in markets such as the U.S. but rarely used in markets like Nigeria. “In The company said that its enterprise-grade solution caters to various companies.

The round was led by Pan-African early-stage venture capital firm, TLcom Capital , with participation from nonprofit Women’s World Banking. So the startup instead partners with banks. Banks provide loans to farmers and make it compulsory for them to have insurance. Image Credits: Pula. million farmers.

We organize all of the trending information in your field so you don't have to. Join 49,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content