This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Oren Yunger is an investor at GGV Capital , where he leads the cybersecurity vertical and drives investments in enterprise IT, data infrastructure, and developer tools. He was previously chief informationsecurity officer at a SaaS company and a public financial institution. So why is compliance alone not enough?

Traditional security approaches have become unsustainable for technology leaders navigating todays complex threat landscape. Information risk management is no longer a checkpoint at the end of development but must be woven throughout the entire software delivery lifecycle.

Data sovereignty and the development of local cloud infrastructure will remain top priorities in the region, driven by national strategies aimed at ensuring data security and compliance. As digital transformation accelerates, so do the risks associated with cybersecurity.

AI and Machine Learning will drive innovation across the government, healthcare, and banking/financial services sectors, strongly focusing on generative AI and ethical regulation. Adopting multi-cloud and hybrid cloud solutions will enhance flexibility and compliance, deepening partnerships with global providers.

However, as more organizations rely on these applications, the need for enterprise application security and compliance measures is becoming increasingly important. Breaches in security or compliance can result in legal liabilities, reputation damage, and financial losses.

As data is moved between environments, fed into ML models, or leveraged in advanced analytics, considerations around things like security and compliance are top of mind for many. In fact, among surveyed leaders, 74% identified security and compliance risks surrounding AI as one of the biggest barriers to adoption.

Financial Institutions Are Facing Growing Security Challenges Financial organisations face unprecedented cybersecurity challenges that threaten their operations, reputation and customer trust. Together, Palo Alto Networks and IBMs experts share their top cybersecurity considerations in a new, compelling vodcast series.

In modern business, cybersecurity is not merely a technical concern but a crucial financial safeguard. With cyber threats growing in sophistication and frequency, the financial implications of neglecting cybersecurity training are severe and multifaceted. The average cost of a data breach ballooned to $4.88

Every tech vendor has to pass security muster with customers, typically a tedious activity involving answering long questionnaires. He knew firsthand from his experience at Kinvey that companies like his had to adhere to a lot of compliance standards, and the idea for the next company began to form in his head.

Droit , a regulatory compliance platform used by finance heavyweights such as Wells Fargo, Goldman Sachs, and UBS, has raised $23 million in a Series B round of funding. And earlier this year, another London-based company called GSS secured $45 million to help banks screen for any sanctions that may have been imposed by governments.

Cybersecurity and systemic risk are two sides of the same coin. Although it was not a security event, the symptoms and responses all fall into the various categories of the cybersecurity program for any company. Systemic risk and overall cybersecurity posture require board involvement and oversight.

As for Kompliant’s second co-founder, Brad Wiskirchen, he was chairman of the board at the Federal Reserve Bank of San Francisco and a member of the interdepartmental working group on finance and technology at the International Monetary Fund. ” Image Credits: Kompliant. . ” Image Credits: Kompliant.

In a world where digital threats loom large, cybersecurity leadership has become paramount. Recognizing the crucial role of cybersecurity leaders in safeguarding the nation’s digital infrastructure, the first edition of the CSO30 Awards recently took place in Dubai, showcasing the cream of the crop in the field.

Plus, Europol offers best practices for banks to adopt quantum-resistant cryptography. Meanwhile, an informal Tenable poll looks at cloud security challenges. government is urging software makers to adopt secure application-development practices that help prevent buffer overflow attacks. This week, the U.S.

a banking-as-a-service (BaaS) platform that aims to build “DeFi for traditional finance,” has raised $16 million in a Series A round of funding led by CM Ventures. From a product architecture standpoint, Productfy has been built “from the ground up,” he said, to operate with multiple banking partners. Productfy Inc. ,

This creates increased regulatory scrutiny, with the risk of massive fines for non-compliance. Or, the UK’s Financial Conduct Authority fining GT Bank £7.8m Or, Solaris , the German Bank-as-a-Service (BaaS) provider slapped with a restriction to not onboard any future clients without government approval. for AML failures.

However, it differentiated itself by committing to payments on social media platforms, which Nigerian digital bank Carbon was interested in when it acquired the startup in 2019. As such, banking-as-a-service platforms see an opportunity to provide more personalized services and flexibility at less cost.

Along with nearly every other industry, banking is facing greater competitive pressure than ever. As banks continue to face this reality, they’re also tasked with addressing a variety of rapidly changing issues, including those surrounding data protection, adoption of cryptocurrency, and anonymizing data (AI models). .

Banks are striving for digital innovation but regulatory constraints, data security and privacy concerns, integration challenges, and the high costs of enabling change prevent 70% from achieving their transformation goals. Overall, the banks digital channel perception CSAT improved from 63% in 2022 to 80% in 2024.

cybersecurity startup CybSafe , a “behavioral security” platform, raised a $7.9 This SaaS product with a per-user-based, subscription licensing model has a “behavior-led” platform that manages people-related security. In other words, it uses behavioral science and data analytics to help employees be more cybersecurity aware.

The generative AI revolution has the power to transform how banks operate. Banks are increasingly turning to AI to assist with a wide range of tasks, from customer onboarding to fraud detection and risk regulation. So, as they leap into AI, banks must first ensure that their data is AI-ready. Generative AI, Innovation

Led by Pacetti, the company was able to reduce many variables in a complex system, like online sales and payments, data analysis, and cybersecurity. “We BPS also adopts proactive thinking, a risk-based framework for strategic alignment and compliance with business objectives.

Two months ago, the Securities and Exchange Commission (SEC) said it had fined 16 Wall Street firms more than $1.1 billion for “widespread recordkeeping failures” regarding maintaining electronic communications, contravening federal securities laws. Keeping up.

Over 90% of the world’s leading banks are either exploring, experimenting (PoCs), or formulating a strategy for leveraging blockchain technology, says an Accenture survey. Benefits of Blockchain in banking. Greater security. Source: Banking on Blockchain. Intra-bank cross-border payments. Areas of impact.

Imagine a bustling bank, made not of bricks and mortar, but of a swirling mass of data in the cloud. Account numbers, transaction histories and personally identifiable information (PII) zip across servers, powering the financial world. Therefore, securing this sensitive information is paramount.

Mohamed Salah Abdel Hamid Abdel Razek, Senior Executive Vice President and Group Head of Tech, Transformation & Information, Mashreq explains how the bank is integrating advanced technologies and expanding its digital footprint. This approach has significantly enhanced the customer banking experience.

Prior to now, Hawk AI had raised $10 million , and with a fresh $17 million in the bank, the company said that it plans to bolster its product development and global expansion plans. Compliance officers need to have transparency over both.” And this is where Hawk AI is setting out its stall.

Reliability and security is paramount. With AI now incorporated into this trail, automation can ensure compliance, trust and accuracy critical factors in any industry, but especially those working with highly sensitive data. Without the necessary guardrails and governance, AI can be harmful.

The Internet of Things has a security problem. The past decade has seen wave after wave of new internet-connected devices, from sensors through to webcams and smart home tech, often manufactured in bulk but with little — if any — consideration to security. Security veteran Window Snyder thinks there is a better way.

As I work with financial services and banking organizations around the world, one thing is clear: AI and generative AI are hot topics of conversation. In the finance and banking industry, however, organizations are seeking extra guidance on the best way forward. Regulatory compliance. In short, yes. But it’s an evolution.

The pandemic has resulted in a shift in consumer behavior that now favors contactless and digital banking options, and with one in four U.S. It needs to be both effective and secure. As more and more retailers make this move, partnering and collaborating with fintechs can help them build, scale and secure their financial offerings.

It’s been a particular challenge for the financial services industry, which has comparatively strict governance and compliance requirements. Securities and Exchange Commission (SEC) fined Wall Street banks, including Bank of America and Goldman Sachs, $1.8 In September, the U.S.

Excitingly, it’ll feature new stages with industry-specific programming tracks across climate, mobility, fintech, AI and machine learning, enterprise, privacy and security, and hardware and robotics. Venture firms advised portfolio companies to move money out of SVB after the bank said it would book a $1.8 Don’t miss it.

Since then, automation has filled the gap in improving customer experience and security. Workflow automation and data analytics are streamlining document management, cross-checking data, assessing for risk, ensuring regulatory compliance, and so on. Security and privacy.

However, as more organizations rely on these applications, the need for enterprise application security and compliance measures is becoming increasingly important. Breaches in security or compliance can result in legal liabilities, reputation damage, and financial losses.

Technology leaders in the financial services sector constantly struggle with the daily challenges of balancing cost, performance, and security the constant demand for high availability means that even a minor system outage could lead to significant financial and reputational losses.

1 - CISA: How VIPs and everyone else can secure their mobile phone use In light of the hacking of major telecom companies by China-affiliated cyber spies, highly targeted people should adopt security best practices to protect their cell phone communications. Dive into six things that are top of mind for the week ending Jan.

The emergence of super-apps offers a unique opportunity for leaders in banking and payments to innovate and expand their reach. Financial institutions can tap into new demographics, prioritizing convenience and seamless banking application experiences. Managing security requirements is paramount.

A mid-sized bank I was consulting with for their data warehouse modernization project finally realized that data isn’t just some necessary but boring stuff the IT department hoards in their digital cave. The bank implemented robust data governance practices to enhance data quality, security, and compliance.

The relationships between banks and fintechs are multi-faceted. Well, today, an announcement by global payments giant Visa is aimed at helping facilitate banks and fintechs’ ability to work together. So literally over $100 billion is going into fintech, which is more than the combined tech budgets of every bank in the U.S.

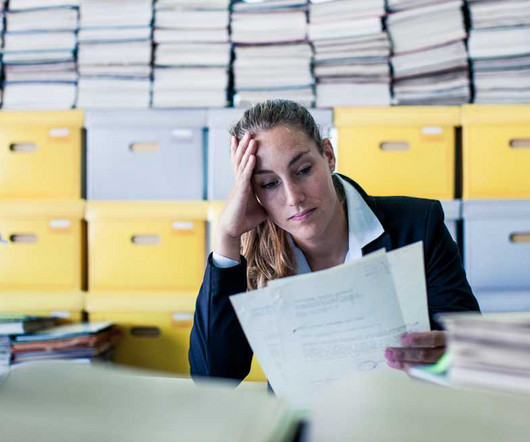

When the chief banking officer of a $10.3B community bank visited a competing super-regional branch in her suburban New Jersey neighborhood, she noticed something troubling. Set amid an open floor plan, the stacks of files left sensitive customer information—business and personal, loans and deposits—available for all to see 1.

Vast amounts of information improve banks’ ability to support customers, but financial institutions must know how to use it. Today’s banking customer is in serious need of guidance from banks, whether it’s about spending, saving, borrowing, planning or all of the above. Key pain points for modern banks.

It enables organizations to extract valuable information from multimodal content unlocking the full potential of their data without requiring deep AI expertise or managing complex multimodal ML pipelines. It adheres to enterprise-grade security and compliance standards, enabling you to deploy AI solutions with confidence.

complex compliance requirements such as the AI Act and crypto taxation policies are demanding startups’ resources. Furthermore, embedded finance will grow as financial services integrate even more heavily into nonfinancial platforms, letting consumers access banking, lending or insurance directly within daily-use apps.

We organize all of the trending information in your field so you don't have to. Join 49,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content